Vietnam Cashews: Stabilizing Prices, Shifting Demand, and El Niño Ahead

7 MIN READ

By Juan Ayala — June 30, 2026

Our Monthly Nuts Market Report blends real-time data with field insights to

support your private label retail strategy.

Want it monthly?

Sign up here

|

Getting your Trinity Audio player ready...

|

What’s Happening This Month?

The global cashew market showed solid structural improvement through June, closing the month in a much stronger position than most buyers anticipated at the start of the year. We are seeing steady demand growth across major import hubs like Europe, China, and the Middle East. Crucially, surplus inventories across the supply chain have leveled out, clearing the heavy oversupply pressure that disrupted the market throughout 2025 and early 2026.

Developments in competing tree nuts are also providing good tailwinds for the cashew sector. Almond demand is bouncing back, pistachio crops look noticeably tighter, walnut stocks are stabilizing, and Brazil nut supplies remain heavily restricted. Because these alternative nuts are facing tighter fundamentals or higher prices, cashews are entering the second half of 2026 in a highly competitive position, setting up a much stronger outlook for demand.

Broader economic headwinds and careful consumer habits mean buyers are still avoiding risky, speculative volumes. However, the general market sentiment has clearly changed. Procurement teams are no longer just buying hand-to-mouth to protect budgets; instead, the focus has shifted toward securing reliable supply pipelines and locking in forward inventory coverage.

Key Market Signals at a Glance

- Grade Performance Resilience: WW180’s and WW240’s continue to represent the strongest-performing premium sectors, while standard WW320’s lines have established a firm floor.

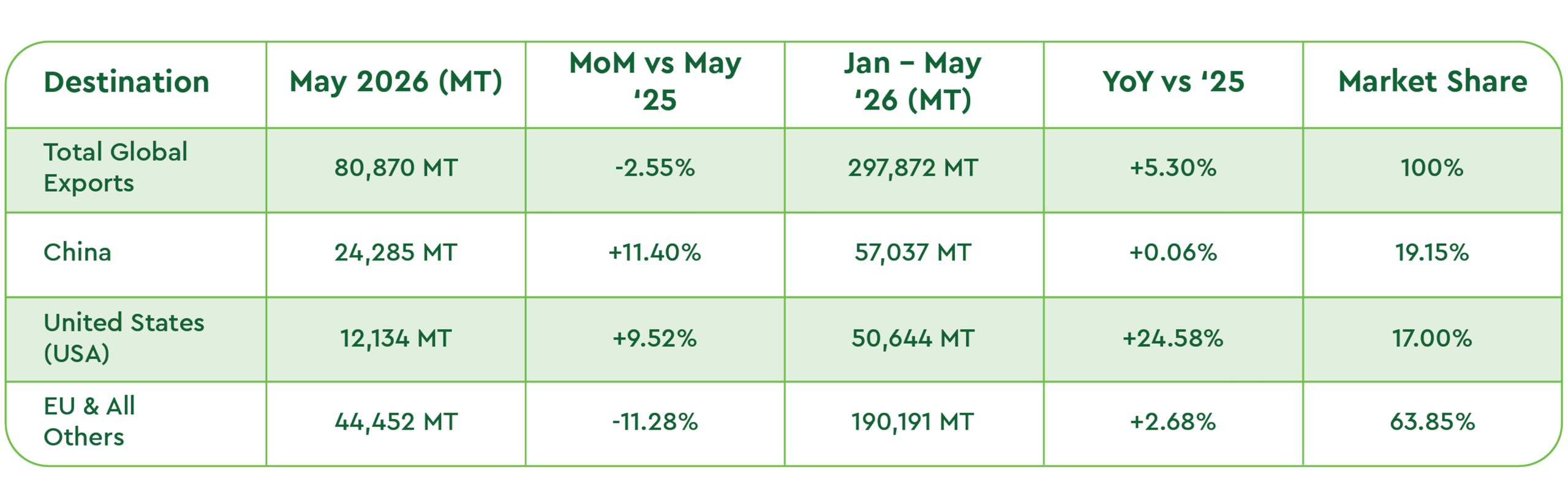

- Geographic Demand Rebalancing: In the first five months of 2026, China officially surpassed the United States as Vietnam’s largest single export destination, anchoring global volume distribution firmly within Asian expansion corridors.

- Macro Destination Recoveries: Despite 2025 declines in US imports caused by tariffs, inflation, and weak consumer confidence, clear indicators of a demand recovery are visible for 2026. Europe maintains moderate, price-driven growth.

- Inbound Cost Adjustments: Kernel prices have ticked up slightly by a few cents in recent days, driven by lower overall crop quality (resulting in higher processing costs), alongside elevated packaging material and ocean freight expenses.

Logistics Advisory: Freight costs continue to weigh heavily on spot execution. Space out of Ho Chi Minh City to Los Angeles (HCM-LAX) remains exceptionally tight, with current spot rates commanding USD 4,000–4,800 per 20’/40′ FCL.

Deep Dive Analysis & Origin Performance

Vietnam Cashew Market Performance

The Vietnamese processing sector demonstrated robust commercial momentum throughout June, driven by steady forward bookings and higher manufacturing overhead:

- WW180 remained the strongest-performing grade, with prices increasing approximately USD 0.10/lb. during the month and reaching around USD 4.20/lb. FOB. Demand remained steady despite higher pricing, reflecting continued interest from premium markets.

- WW240 also maintained strong support. Buying activity concentrated around USD 3.45–3.55/lb. FOB, with many processors withdrawing offers due to limited availability. The combination of healthy demand and disciplined selling behavior helped keep the market firm.

- WW320 showed signs of recovery after several months of pressure. Demand improved gradually throughout June and offers for good-quality EU-grade products increased to approximately USD 3.15/lb. FOB. Geopolitical risk adds volatility, not certainty.

- WS and LP remains stable at 2.5–2.6 USD/lb. and 1.9–2.00 USD/lb.

Vietnamese Cashew Kernel Export Figures (May 2026)

Source: Vietnam Cashew Association Data

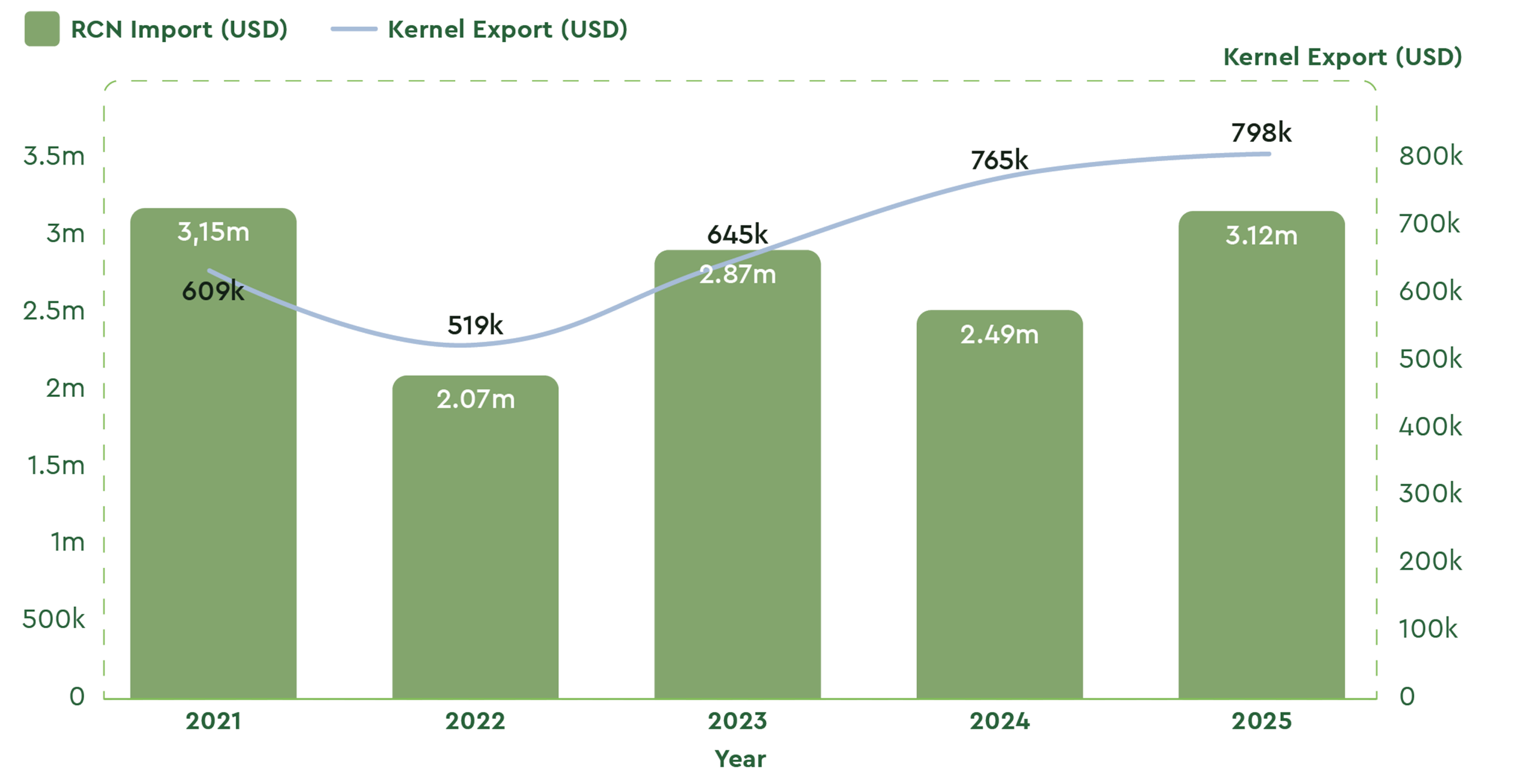

Vietnam RCN import and RCK export 2021–2025: Kernel exports have grown steadily from $609K (2021) to $797K (2025), even as RCN imports fluctuate, reflecting improving processing efficiency and value-add capacity.

Source: Vinacas Cashew Association at INC Conference 2026.

West African Raw Material Dynamics & Processing Pressures

The 2026 West African harvest has extended longer than normal, with collection rolling through Guinea-Bissau, Senegal, and Côte d’Ivoire. While total volumes are high, processors are facing lower overall raw cashew nut (RCN) quality compared to last year’s exceptional crop:

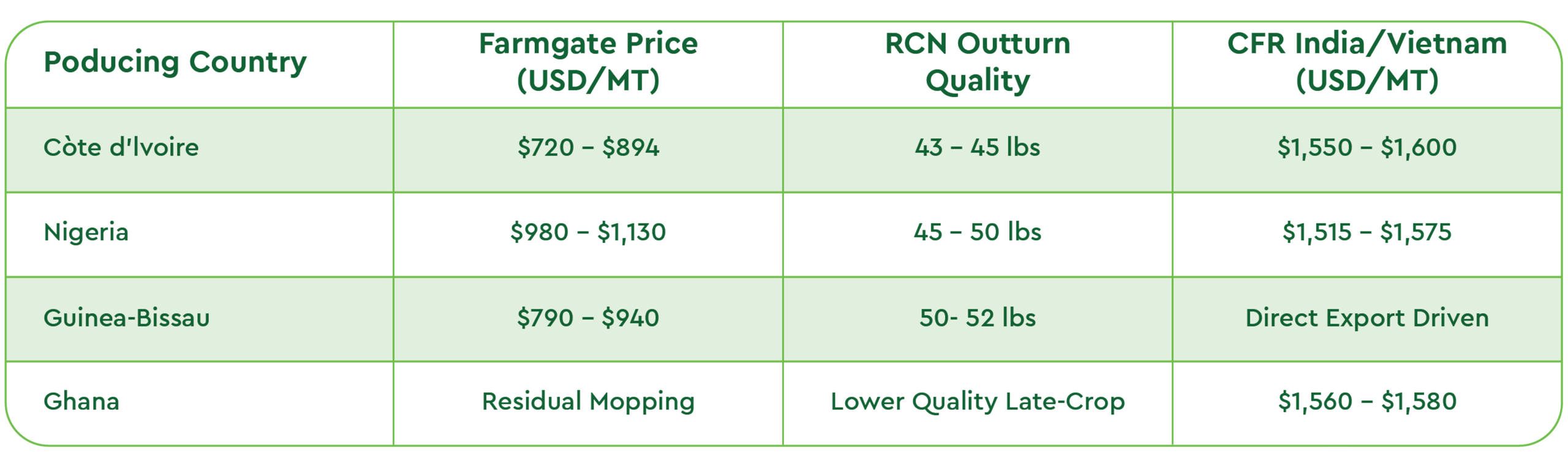

- Côte d’Ivoire: Commercialized volume is approaching 1.3 million tons and is expected to exceed this benchmark by July. However, the late-harvest crop circulating in the market features lower outturns, averaging 42–45 lbs, compressing processor margins.

- Guinea-Bissau: Trading remains highly competitive with roughly 150,000 tons commercialized. Farmgate prices have moved up to USD 790–940/MT on strong buyer interest, though quality remains high with outturns at 50–52 lbs.

- Nigeria: The farmgate season has largely concluded, shifting volume focus to warehouses. Trade estimates place the total crop at 350,000 to 400,000 tons, bolstered by cross-border inflows from Benin.

Middle East tensions may affect logistics and short-term demand, but fiscal resilience in Gulf economies limits uniform downside risk.

International Raw Cashew Nut (RCN) Price Matrix (June 2026) and processing status

Africa’s local processing share is rising steadily, from 16.4% in 2024 to 18.8% in 2025, with a projected leap to 26.4% in 2026. Total processed volume is set to nearly double from 513,000 MT to 920,000 MT in just two years.

Sources: CCA, CCF, TCDA, NCAN, ACA, trade sources, Cashew information research, CBT-Tanzania, IAM-Mozambique. *2026 projected.

Macro Risk Factors: The El Super Niño

While the current cashew supply is stable after a good harvest, El Niño introduces clear long-term risks. Major climate agencies, including NOAA and the WMO, project an 82% probability of this weather pattern through July 2026, rising to a 96% probability between December 2026 and February 2027.

For procurement teams, the main risk is timing. If adverse weather occurs during key crop development stages in West Africa and Southeast Asia, raw material quality will decline.

Adverse conditions directly degrade raw material consistency, leading to smaller average nut sizes, lower kernel outturn ratios (KOR), and higher moisture-related processing defects.

During these types of climate risks, we like to reinforce the importance of:

- Supplier diversification

- Long-term sourcing partnerships

- Strategic inventory planning

- Sustainable agricultural investment

Final Thoughts on Strategic Procurement

June 2026 brings renewed confidence to the nut industry. While a massive price spike is unlikely, prices have hit a stable floor.

Demand is growing, raw material supply is steady, and expensive alternative tree nuts make cashews highly competitive. For retail buyers, the time to wait out the market has passed; the immediate priority is securing forward coverage.

Long-term supply chain security now requires adapting to climate risks. The industry is well-positioned to meet this rising demand, but long-term climate change has turned climate resilience into a significant competitive advantage. To protect against unpredictable crop yields, companies must focus on multi-origin diversification and sustainable sourcing infrastructure.

Ultimately, the second half of 2026 will be driven by four themes: stronger retail demand, tight stocks in competing nuts, growing African processing, and climate volatility. Prices will likely firm up gradually rather than weaken, favoring private label programs that partner with origin-integrated suppliers.

The private-label sourcing strategy at Certified Origins is specifically engineered to help our partners successfully maneuver through this evolving market environment.

Reach out to our procurement and sourcing specialists today to discuss how we can build supply resilience across your nut category programs and ensure volume continuity through the remainder of 2026.

Primary Origin Intelligence & Field Verification: Mai Phan, Vietnam Country Supervisor, Certified Origins.

Meteorological Modeling: NOAA Climate Prediction Center

Macro Commodity Risk Analysis: Rotterdam Commodity Insights

West African Crop & Price Tracking: African Cashew Alliance, AfriCashewSplits Week 23–24

Vietnam Cashew Association (VINACAS) (2026) Vietnam Cashew Export Statistics and Market Information May 2026 Edition.

Share on