Pressure on Producers Persists Alongside Trade Volatility

5 MIN READ

By Franziska Finck — June 26, 2026

Our Monthly Olive Oil Market Report blends real-time data with field insights to

support your private label retail strategy.

Want it monthly?

Sign up here

|

Getting your Trinity Audio player ready...

|

What’s Happening This Month?

This month, the olive oil market is characterized by a broad price decline across Spain and Italy. In Spain, origin prices continued to ease despite indicators of resilient underlying demand and lower-than-expected stock levels. In Italy, quotations have also dropped significantly from the highs recorded late last year, pressured by abundant domestic inventories and international competition.

Simultaneously, market attention is focused on emerging geopolitical trade risks. Recent news that the US has proposed additional tariffs on imports from 60 economies over forced labor concerns has introduced a new layer of uncertainty. While the implementation timeline and exact impact remain fluid, this development creates potential challenges for global exporters regarding long-term stability and competitive positioning in key North American markets.

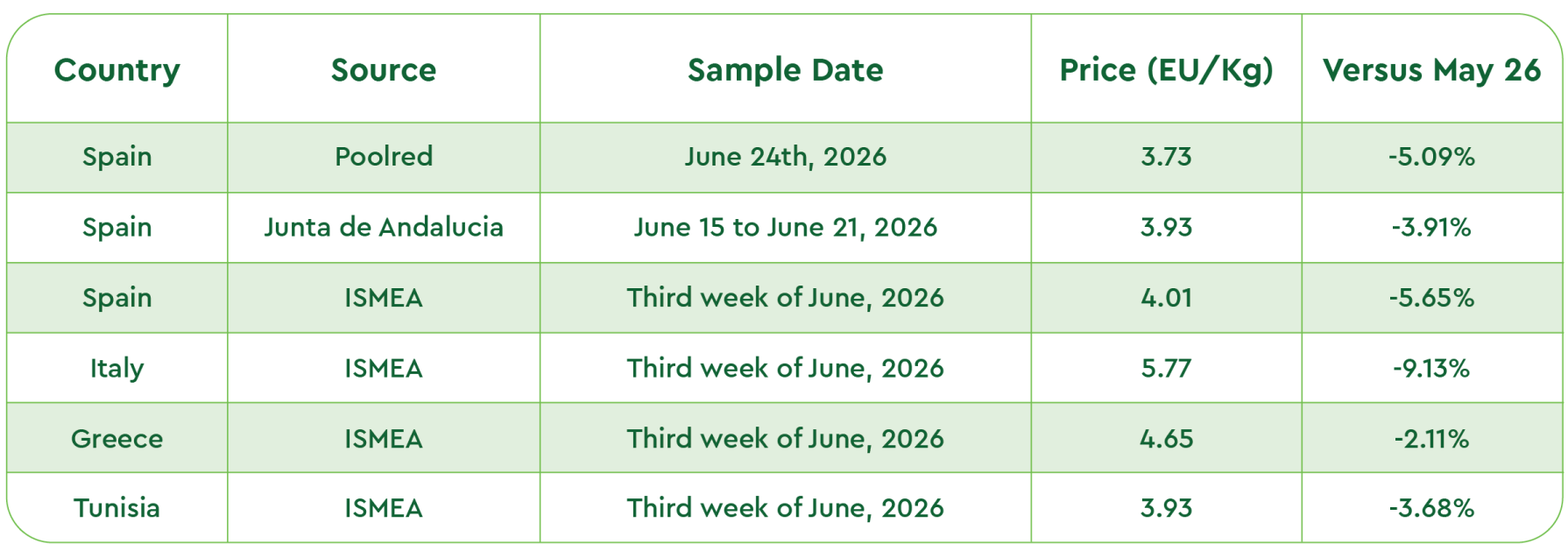

A look at the major trading platforms today shows the following picture:

Note: Reported prices are averages across multiple quality grades. Premium, traceable, clean, pesticide-free extra virgin olive oil typically trades at higher values.

Latest Olive Oil Market Figures from Official Industry Sources

Sources: Poolred, Ismeamercati

Spanish Olive Oil: Revised May Data Challenges Recent Price Fluctuations

Recent data updates from Spain’s Food Information and Control Agency (AICA) have caused short-term volatility in market assessments. While initial AICA figures for May indicated market releases of only 73,644 tons (export and national) the revised official data corrected this volume to approximately 100,352 tons. This upward revision fundamentally alters the short-term outlook, confirming that underlying demand remains robust.

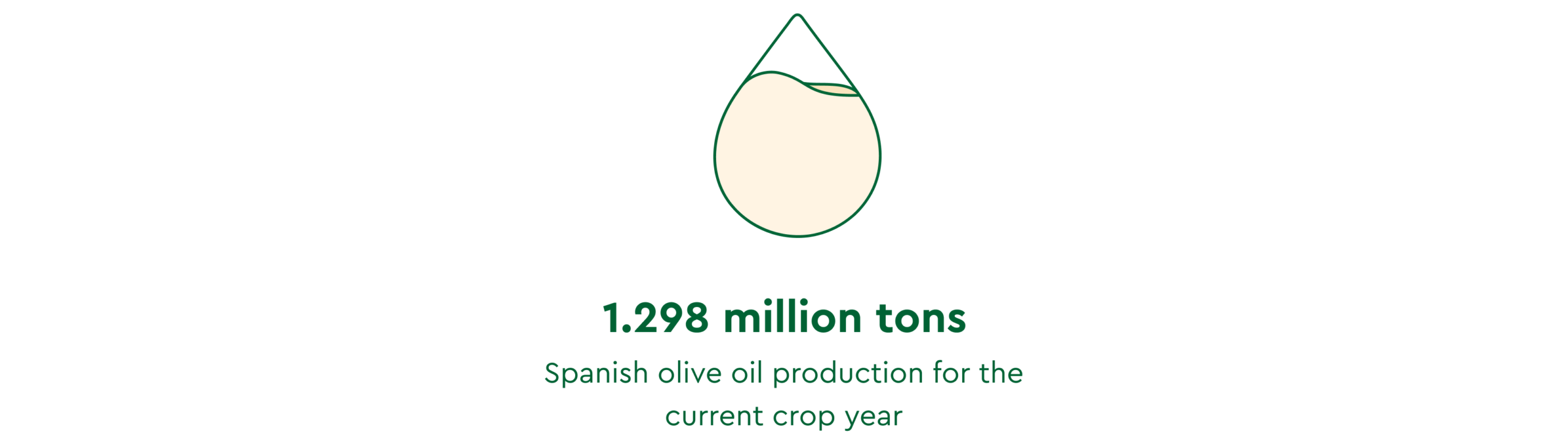

According to the Ministry of Agriculture, Fisheries and Food (MAPA), Spanish olive oil production for the current crop year stands at approximately 1.298 million tons. By the end of May, around 977,000 tons had been marketed. Concurrently, AICA revised total olive oil stocks downward to 774,988 tons, with roughly 507,000 tons held directly by olive mills.

The correction of the figures has also raised concerns within the sector. The initially published data contributed to market uncertainty and led many operators to question the reliability of the statistics.

Industry insiders suggest this misalignment stems from reporting inaccuracies or technical lapses in processing inventory and trade flow figures. However, a comprehensive clarification regarding these statistical deviations has yet to be officially released.

Italian Olive Oil Prices Drop Amid High Stocks and Market Pressure

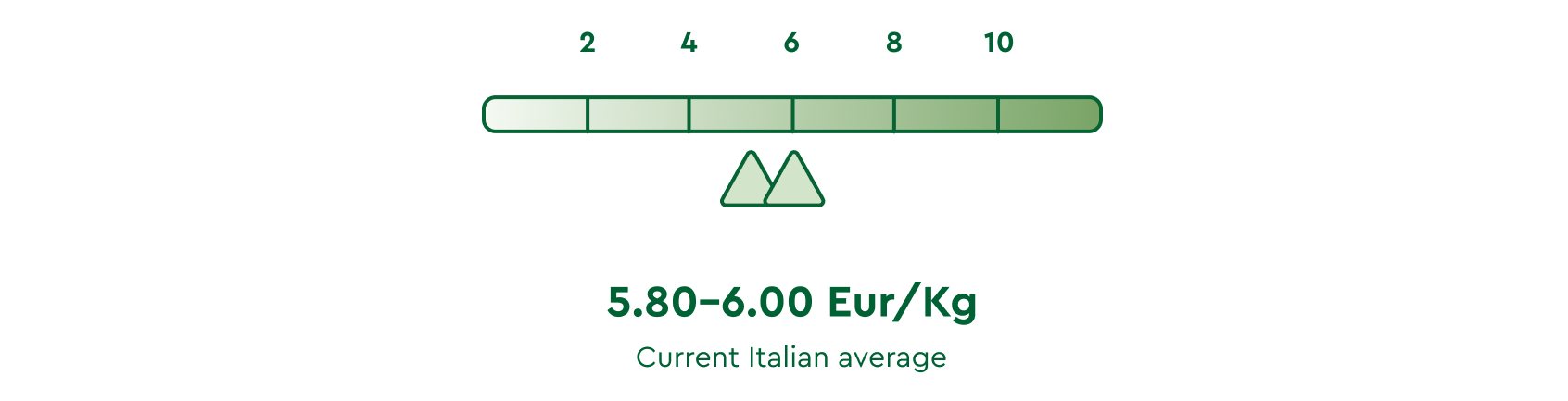

The Italian olive oil sector is currently facing downward price pressure. According to ISMEA, buyers were paying around 8.00 Eur/Kg for Italian extra-virgin olive oil late last year; however, current transactions average 5.80–6.00 Eur/Kg, depending on quality parameters. This represents an approximate 37% year-on-year decline.

This price adjustment is heavily influenced by domestic supply levels.

Official data from the ICQRF Frantoio Italia report indicates that as of May 31, 2026, total Italian inventories reached approximately 277,000 tons. This includes 221,800 tons of extra-virgin olive oil, of which 132,700 tons are Italian-origin EVOO. Overall stock levels are roughly 45% higher than the previous year.

Simultaneously, imported olive oils from lower-cost-producing regions continue to affect domestic valuations. Agricultural institutions warn that current prices are increasingly falling below the breakeven threshold for traditional olive growers, undermining the economic sustainability of local operations.

To combat unfair practices such as the commercialization of “soft deodorized” olive oils and blends of unidentified origin, Italian farmers and producers are demanding stronger enforcement of global quality standards and greater supply chain transparency.

They are specifically advocating for the use of Nuclear Magnetic Resonance (NMR) spectroscopy and isotopic mapping as official scientific methods for verifying geographical origin and extra-virgin quality standards.

Global Consumption Shifts and Long-Term Market Demographics

According to long-term industry reports featured in Olimerca and statistical indicators from the International Olive Council (IOC), global olive oil consumption is projected to increase by 14% to 20% by 2050. This trajectory represents an additional structural demand of approximately 500,000 to 700,000 tons per year.

This volumetric expansion is driven primarily by non-producing import markets, specifically the United States, Brazil, and Canada, which counteract a minor, long-term consumption contraction within traditional Mediterranean producing nations.

Currently, baseline institutional data segments global consumption across three primary categories:

- 50%: Major producing nations (Spain, Italy, Greece, Portugal, Morocco, and Turkey)

- 30%: Nations with emerging or limited domestic production (including the US, Brazil, and Australia)

- 20%: Import-dependent markets with negligible or no domestic cultivation (e.g., Germany, Canada, United Kingdom)

Market distribution data indicate that approximately 75% of total volume is consumed within domestic households, while 25% moves through foodservice and commercial channels. Behavioral studies confirm that utilization remains heavily concentrated in cold preparations:

- 49% for direct seasoning and flavor enhancement

- 26% for dressings and marinades

- 25% for high-temperature frying and roasting

The primary purchasing demographic in expanding import markets continues to trend toward middle- to high-income households over the age of 49.

Macroeconomic Impact: Rising Input Costs and Global Logistics

Across primary Mediterranean growing regions, input costs for specialized pesticides, fertilizers, tractor diesel, and industrial electricity have escalated. According to institutional data from agricultural bodies, these factors have increased baseline farming expenses by more than 200 Eur per hectare, setting an elevated production price floor for growers.

Because the fastest-growing consumer markets are located overseas (e.g., North America and the Asia-Pacific region), elevated maritime freight rates, fuel surcharges, and transit insurance continue to affect retail costs, suppressing consumption.

Even when bulk-origin prices soften in producing countries, tariffs, shipping, and supply chain costs can keep shelf prices elevated in non-producing importing countries.

Final Thoughts on Strategic Procurement: Pricing and Global Trade Dynamics

The current market exhibits a clear pricing divergence: robust underlying demand and declining stock levels in Spain have not prevented a broad decrease in origin prices. With valuations falling near or below farmers’ minimum production costs, the market risks structural imbalances that could trigger future price corrections.

Looking ahead, the market is factoring in a positive outlook for the upcoming harvest. Recent field assessments by our procurement team in Spain align with preliminary institutional expectations from regional agricultural bodies. Inspections across 13 olive groves in Jaén and Córdoba indicate healthy agronomic conditions.

Tree loads in Jaén remain consistent at 70–75%, while Córdoba exhibits greater variance (20–80%). Production is projected to increase by approximately 50% in Jaén and 30% in Córdoba year-on-year, supporting a preliminary Spanish crop forecast of 1.7–1.8 million tons.

Although the present outlook remains positive, definitive production totals will depend on how the crop fares during the upcoming peak summer heat.

Reach out to the Private Label and sourcing specialists at Certified Origins to explore strategies to manage shifting trade dynamics and ensure the stability of your supply chain.

Sources:

Poolred,

Ismea Mercati,

Junta de Andalucia,

Teatro Naturale,

International Olive Oil Council

Share on