Slow Activity and Down-Pressures in the Olive Oil Market

6 MIN READ

By Franziska Finck — May 27, 2026

Our Monthly Olive Oil Market Report blends real-time data with field insights to

support your private label retail strategy.

Want it monthly?

Sign up here|

Getting your Trinity Audio player ready...

|

What’s Happening This Month?

The Spanish and Italian olive oil markets are currently experiencing very low level of activity. Following weak spring figures, uncertainty continues across the entire value chain as bottlers, supported by high inventory levels, show little urgency to secure additional volumes.

This liquidity gap highlights a clear dynamic: industrial buyers are choosing to stay on the sidelines, waiting for the critical May flowering to dictate the next price trend, while Mediterranean producers are resisting further downward pressure to protect their margins from rising operating expenses, driven up by energy and fertilizer costs.

In this context of slow transactions, current quotations on platforms like ISMEA and Poolred are best understood as general guidelines. Low trading volumes and complex contract structures create a reporting lag, meaning these figures reflect broad market sentiment rather than real-time data.

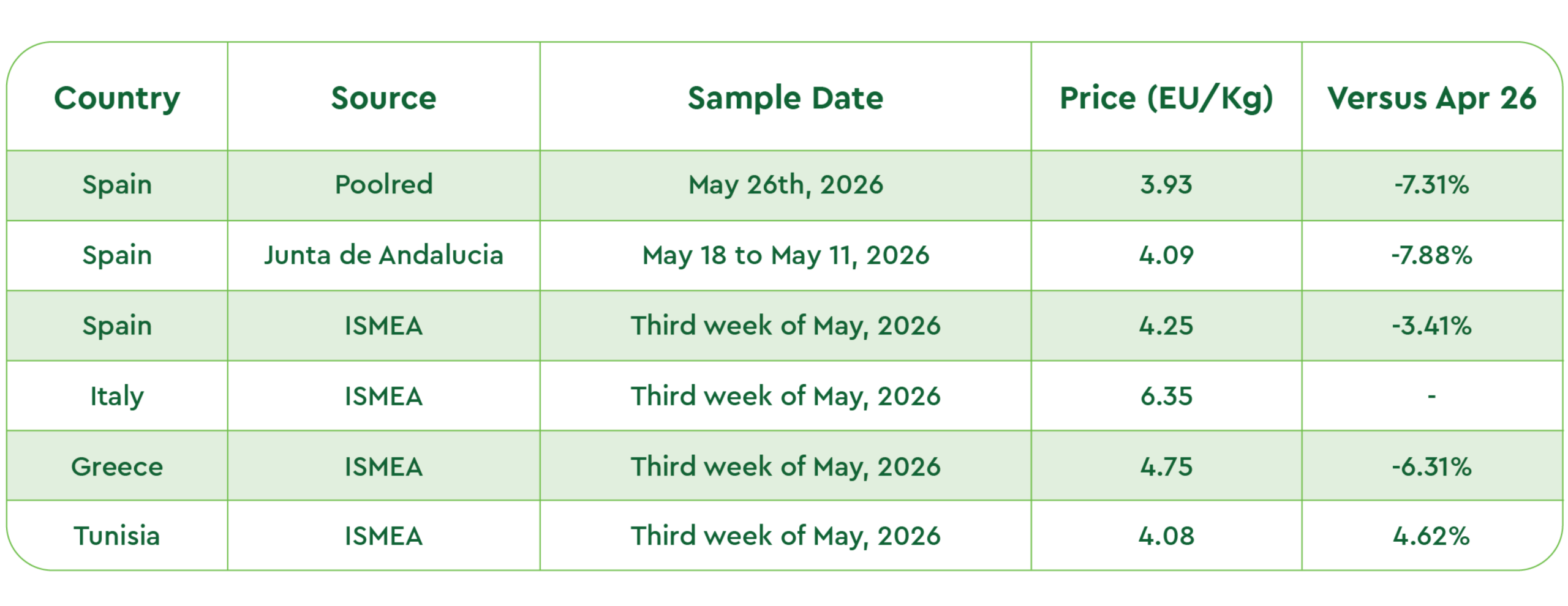

A look at the main market pools currently shows the following picture:

Note: Reported prices are averages across multiple quality grades. Premium, traceable, clean, pesticide-free extra virgin olive oil typically trades at higher values.

Note: Reported prices are averages across multiple quality grades. Premium, traceable, clean, pesticide-free extra virgin olive oil typically trades at higher values.

Sources: Poolred, Ismeamercati

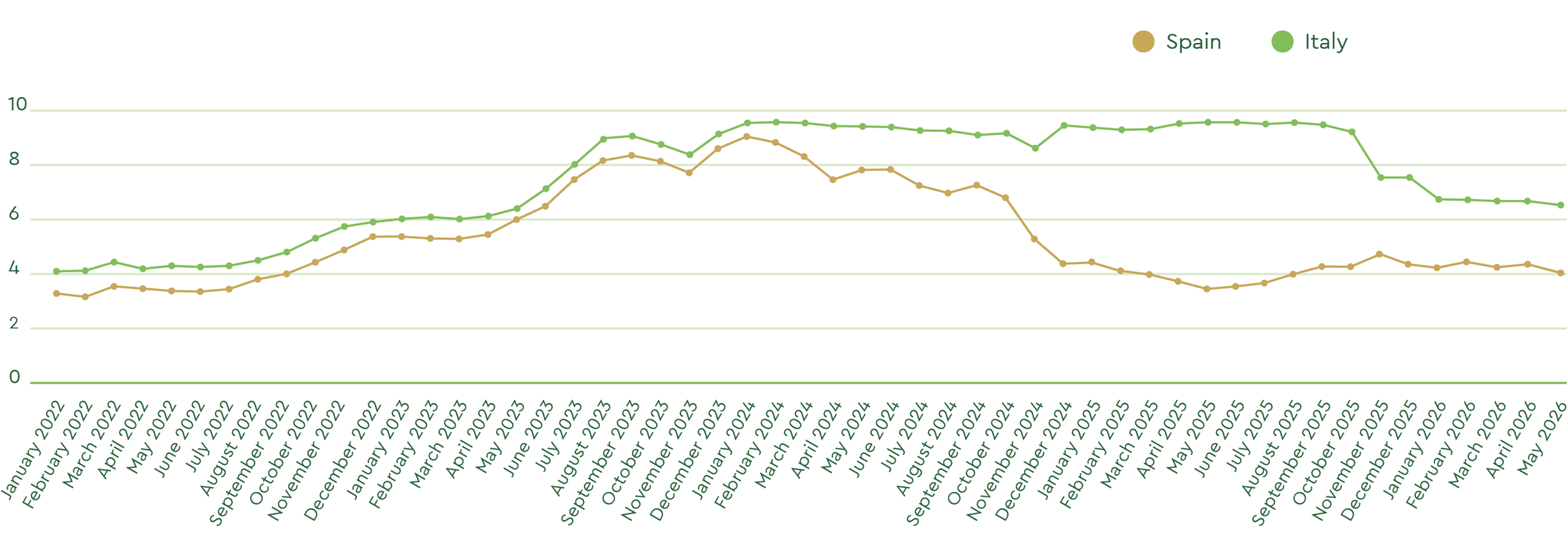

Extra Virgin Olive Oil Price Evolution 2022-2026

Sources: Poolred, Ismeamercati

Spain & Italy: April Production, Demand & Stocks

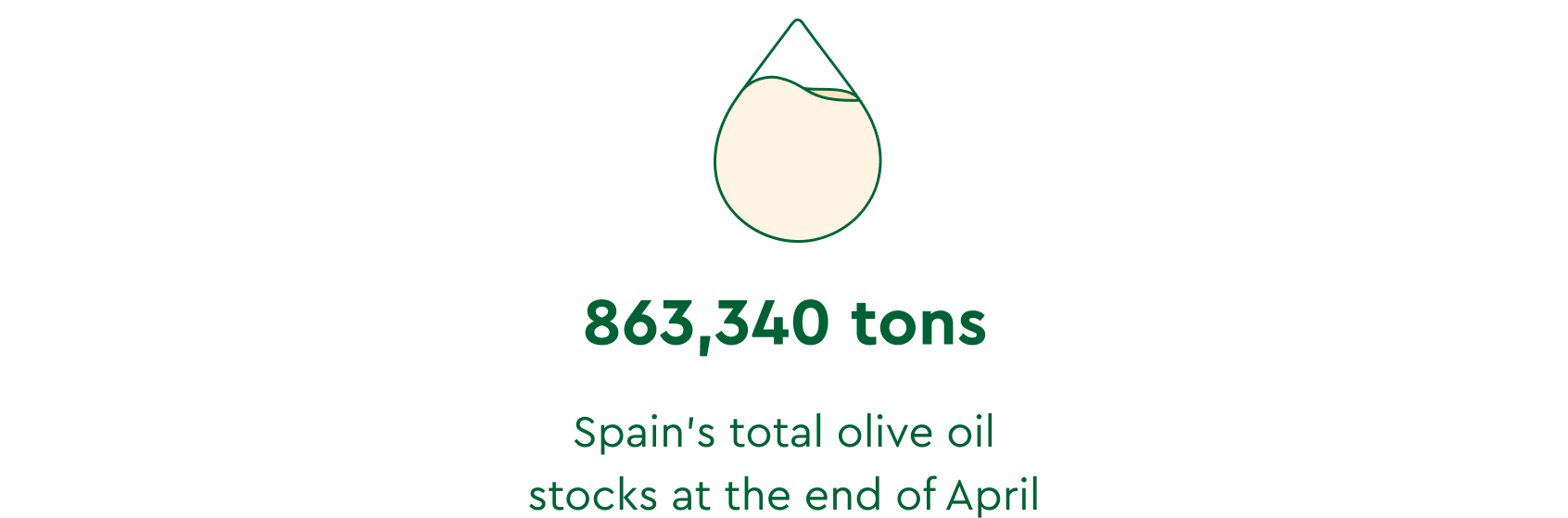

The Spanish olive oil campaign 2025/26 has recorded a cumulative production of 1,294,590 tons through April, according to the specialized portal Mercacei, citing AICA data. In terms of remaining physical inventory, Spain’s total stocks currently stand at 863,340 tons, with 600,270 tons held in oil mills, 254,326 tons in bottling plants, and 8,744 tons in communal storage (Patrimonio Comunal Olivarero).

Regarding market sales (exports and domestic consumption), the trade magazine Olimerca describes the April figures for Spain as a clear “disappointment,” as they reached only 93,664 tons (excluding imports), falling significantly short of expectations.

This sharp decline is primarily attributed to lower commercial activity during the Easter holiday week, as well as to lower-cost olive oil from Tunisia and Morocco weakening global demand for Spanish-origin olive oil.

If the projected import volume of around 20,000 tons is confirmed, total sales would barely reach 120,000 tons, a severe drop compared to previous months, which saw market sales of around 141,000 tons and 135,000 tons, respectively. Against this backdrop, the industry’s focus shifts to sales performance in the coming months, with initial estimates suggesting monthly sales could settle at around 100,000 to 105,000 tons, leaving final season-ending stocks at approximately 330,000 tons.

In parallel with this slowdown in Spain, the Italian market is experiencing a clear compression in demand, as evidenced by vastly larger inventory buffers than last year.

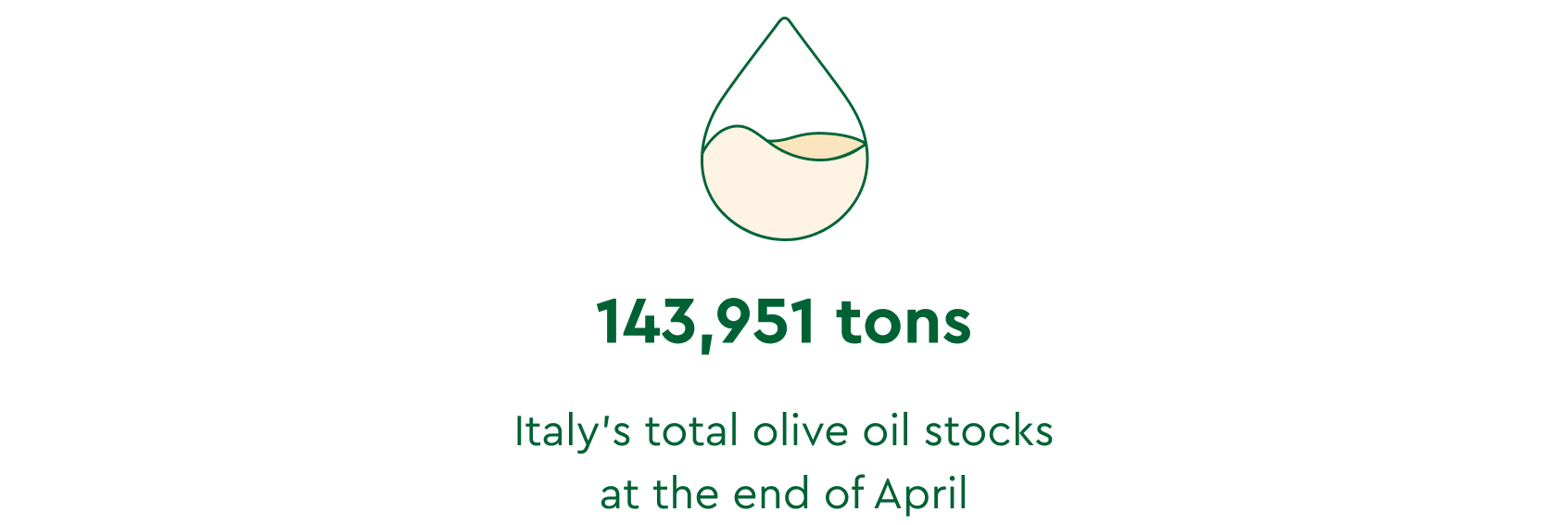

According to the latest Frantoio Italia data citing the Ministry of Agriculture, Italy’s total olive oil stocks at the end of April climbed to 143,951 tons. This volume is virtually double the historically depleted reserves held during the exact same period in 2025.

As in Spain, this volume availability, paired with very quiet market demand, is driving a gradual price deflation, particularly across regional wholesale hubs in the south, where averages have begun to slide below previous baselines.

The Greek olive oil industry faces reduced output and declining prices.

An interesting article from Olive Oil Times recently reported on the difficult situation currently affecting the Greek olive oil market following the completion of the 2025/26 harvest.

Greek olive oil production came in at below 200,000 tons, significantly lower than expected. According to the International Olive Council (IOC), Greek olive oil production in recent crop years developed as follows: 2024/25: 250,000 tons (provisional), 2023/24: 192,000 tons, 2022/23: 345,000 tons, and 2021/22: 232,000 tons. Therefore, a crop of around 200,000 tons would be -20% below the average production of the last five years, estimated at approximately 255,000 tons.

At the same time, producers are facing strong pressure from low producer prices, which are currently around 30% below last year’s levels. In key producing regions such as Crete, Laconia and Messenia, extra virgin olive oil prices are currently ranging between approximately 4.50 Eu/Kg and 5.40 Eu/Kg.

Many producers are holding back their stocks in the hope that wholesale prices will improve over the coming months. Rising production costs, lower yields, and quality challenges caused by the prolonged rainy season and increased pest pressure are adding further strain on the sector.

Cheaper olive oil imports from Tunisia are also continuing to put pressure on the market. Spanish and Greek market participants have particularly criticized the growing volumes of Tunisian olive oil entering the European market and concerns regarding insufficient traceability.

This year’s harvest on Crete dropped significantly to around 45,000-50,000 tons compared to the previous season. Production in Messenia also declined considerably. According to industry experts, only part of this year’s production achieved “Virgin” or “Extra Virgin” quality standards.

Despite the currently challenging market conditions, some producers remain cautiously optimistic about the 2026/27 harvest, as olive trees are reportedly showing good flowering conditions and favorable weather could support a stronger crop next season.

Italy and Spain’s competition in the Global Olive Oil Trade

According to a recent Olimerca report, based on Eurostat data, Italy continues to defend its strong international trade position despite intense competition from Spain and other countries. This underscores a clear value-versus-volume dynamic rooted in the structural production of both nations.

Under normal conditions, Spain acts as the global volume engine, producing roughly 1.3 million tons annually (nearly 45% of world supply). By contrast, Italy produces a limited premium tier of 270,000 to 300,000 tons. Because this output covers less than half of its packaging commitments, Italy operates with a permanent structural deficit, cementing its role as the world’s primary blending and packaging hub that imports a five-year average of 318,745 tons annually from its European neighbors.

Export data from the first five months of the current campaign highlights how these crop baselines translate into market power. Spain exported 157,000 tons to non-EU destinations (with 50,000 tonnes targeting the U.S.) and 177,155 tons within the EU. Italy exported 79,600 tons to non-EU markets, with the U.S. absorbing over 33,000 tons and the UK 7,000 tons, while moving just 36,515 tons within the EU.

While Spain dominates in terms of volume, Italy leverages its role as a global bottling hub and as home to brands that can command premium shelf space in higher-margin retail sectors.

Final Thoughts on Strategic Procurement: Pricing and Global Trade Dynamics

While weak April sales and media optimism regarding the 2026/27 harvest forecast are currently driving down daily spot prices, industry experts argue that this trend reflects market psychology and panic selling rather than an actual physical oversupply of olive oil.

Market fundamentals remain exceptionally tight; following two historically poor seasons, the current crop represents only a partial recovery, not a comfortable surplus. Meanwhile, global demand remains resilient, with total campaign sales reaching approximately 870,000 tons and exports up 5% year-on-year.

With this in mind, the 4.00 Eu/Kg price levels seen on Poolred today sit below actual production costs. Insiders criticize how isolated, low-volume transactions on public platforms are having a disproportionate, distorting impact on price tracking.

Supporting this view, agricultural associations strongly urge caution against premature price cuts based on speculative 2026/27 forecasts. They warn that such artificial downward spirals threaten the financial survival of farmers before summer weather risks are settled and any new harvest is even produced.

In this context of temporary price compression and tension at the source, the European Union is establishing new market opportunities for the years to come for both high-volume trade and premium PGI/PDO-certified products.

This expansion is led by the EU-Mercosur interim agreement, which opens a market of 700 million consumers and protects over 340 Geographical Indications (GIs). As well as by a revamped EU-Mexico agreement eliminating olive oil tariffs, a newly finalized EU-India pact phasing out duties over five years, and active, tariff-free pathways into Australia and Chile.

North America remains a vital market. While U.S. demand for premium EVOO is stable, fiscal uncertainty persists. The end of temporary 10% U.S. duties and a Department of Commerce probe will likely lead to new permanent tariffs.

Global strategic procurement teams should view these concurrent shifts in sourcing, trade corridors, and regional regulations as a clear signal to reassess traditional procurement models. Future strategies must consider long-term planning rather than reacting to short-term spot-market volatility.

Reach out to the Private Label and sourcing specialists at Certified Origins to explore strategies for managing these shifting trade dynamics and ensuring the stability of your supply chain.

Mercacei,

Olimerca,

Eurostat data,

Poolred,

Ismea Mercati,

Junta de Andalucia,

Teatro Naturale,

International Olive Oil Council

Share on