Trade Pause: Waiting for 2026/27 Crop Insights

6 MIN READ

By Franziska Finck — April 30, 2026

Our Monthly Olive Oil Market Report blends real-time data with field insights to

support your private label retail strategy.

Want it monthly?

Sign up here

|

Getting your Trinity Audio player ready...

|

What’s Happening This Month?

Evaluations for olive oil remain stable and within the current range in Spain and other producing areas, showing limited fluctuations. The market exhibits a balanced supply-demand equilibrium and subdued trading activity as participants await definitive production signals for the next cycle.

Farmers’ and producers’ attention is focused on the second quarter, as the olive tree flowering phase in May and June will offer a first clear insight on what to expect from the 2026/27 harvest.

Recent rainfall has significantly improved growing conditions across Andalusia and Extremadura, supporting positive yield expectations for the upcoming campaign.

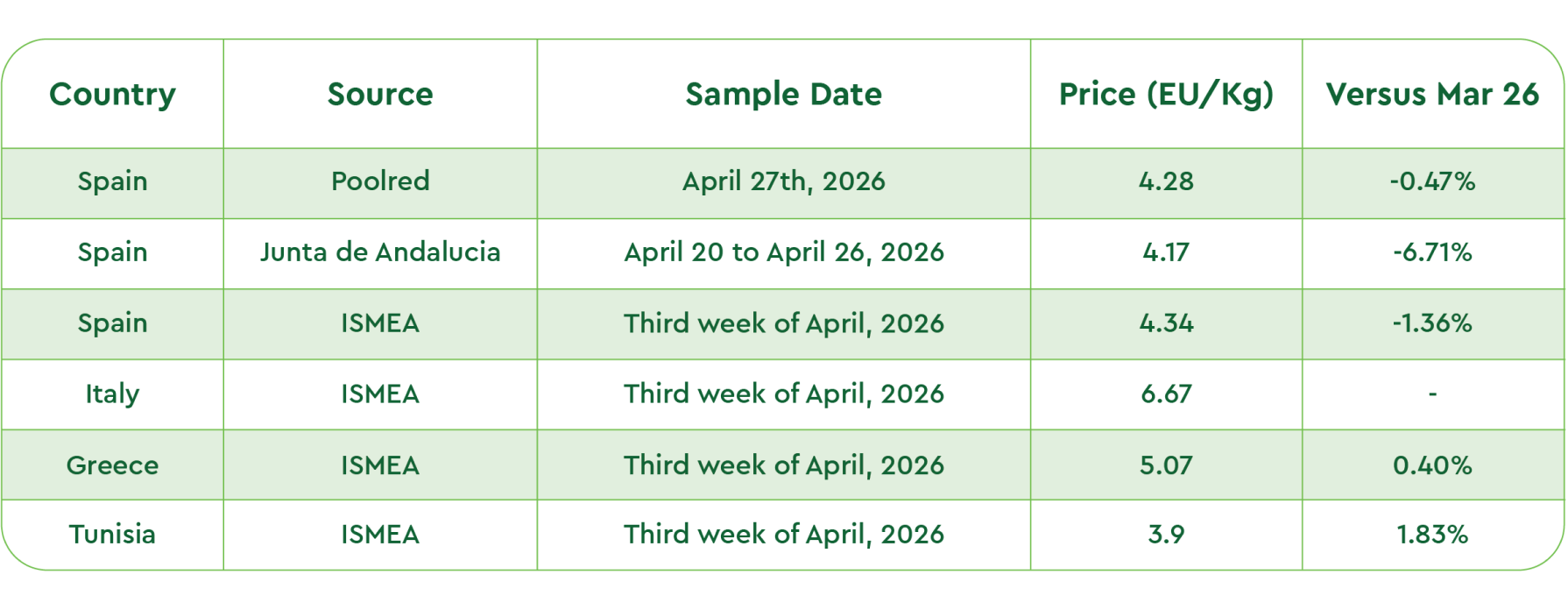

On prices, the market maintains stable levels compared to the previous report: Spanish conventional extra virgin olive oil is trading at 4.2–4.5 Eu/Kg. Italian Evoo remains at a premium at 6.5–7.0 Eu/Kg, supported by tighter supply and strategic inventory management ahead of the new harvest.

In Greece, prices have edged up by 0.05–0.10 Eu/Kg despite overall low trading activity. Tunisia is currently quoted at 3.8–4.0 Eu/Kg, reflecting supply pressure from a high-production campaign and competitive export conditions.

Overall, the market remains in a consolidation phase with distinct price segmentation between origins. The flowering phase will be the primary market driver and volatility catalyst for the 2026 outlook.

Latest Olive Oil Market Figures from Official Industry Sources

Note: Reported prices are averages across multiple quality grades. Premium, traceable, clean, pesticide-free extra virgin olive oil typically trades at higher values.

Note: Reported prices are averages across multiple quality grades. Premium, traceable, clean, pesticide-free extra virgin olive oil typically trades at higher values.

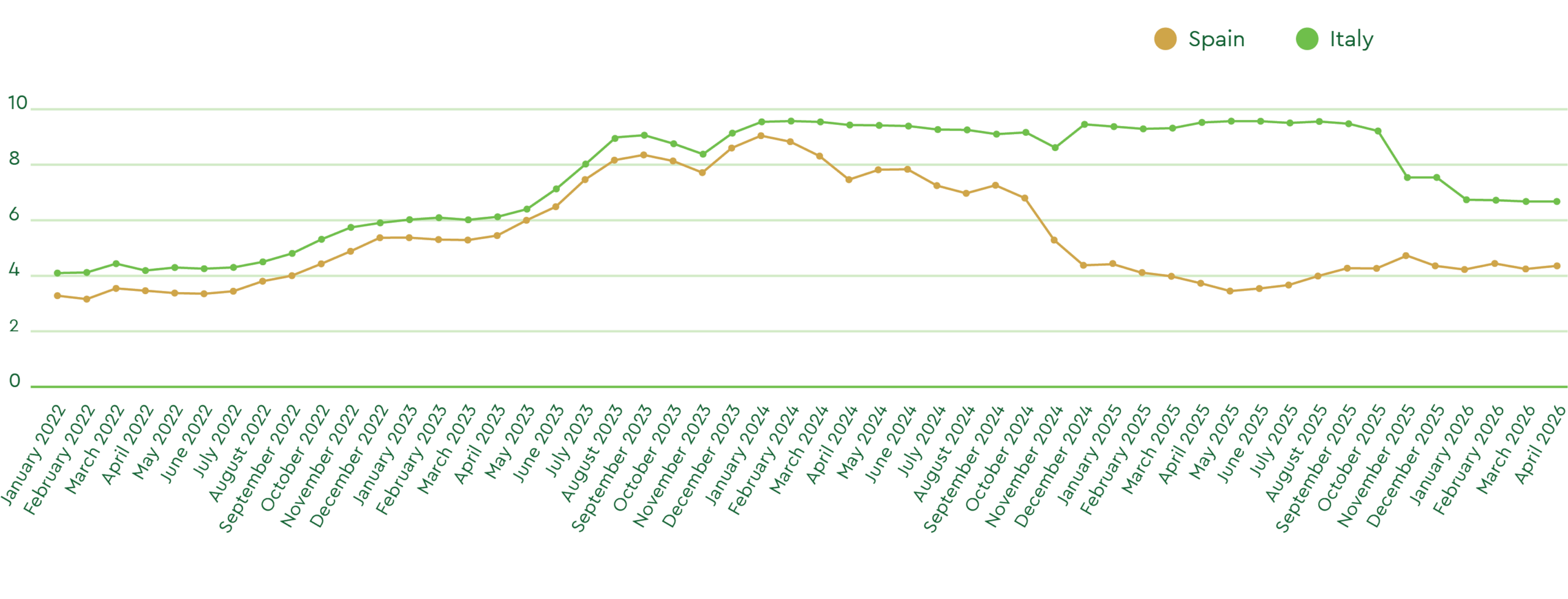

Extra Virgin Olive Oil Price Evolution 2022-2026

Sources: Poolred, Ismeamercati.

Sources: Poolred, Ismeamercati.

Spain & Italy: March Production, Demand & Stocks

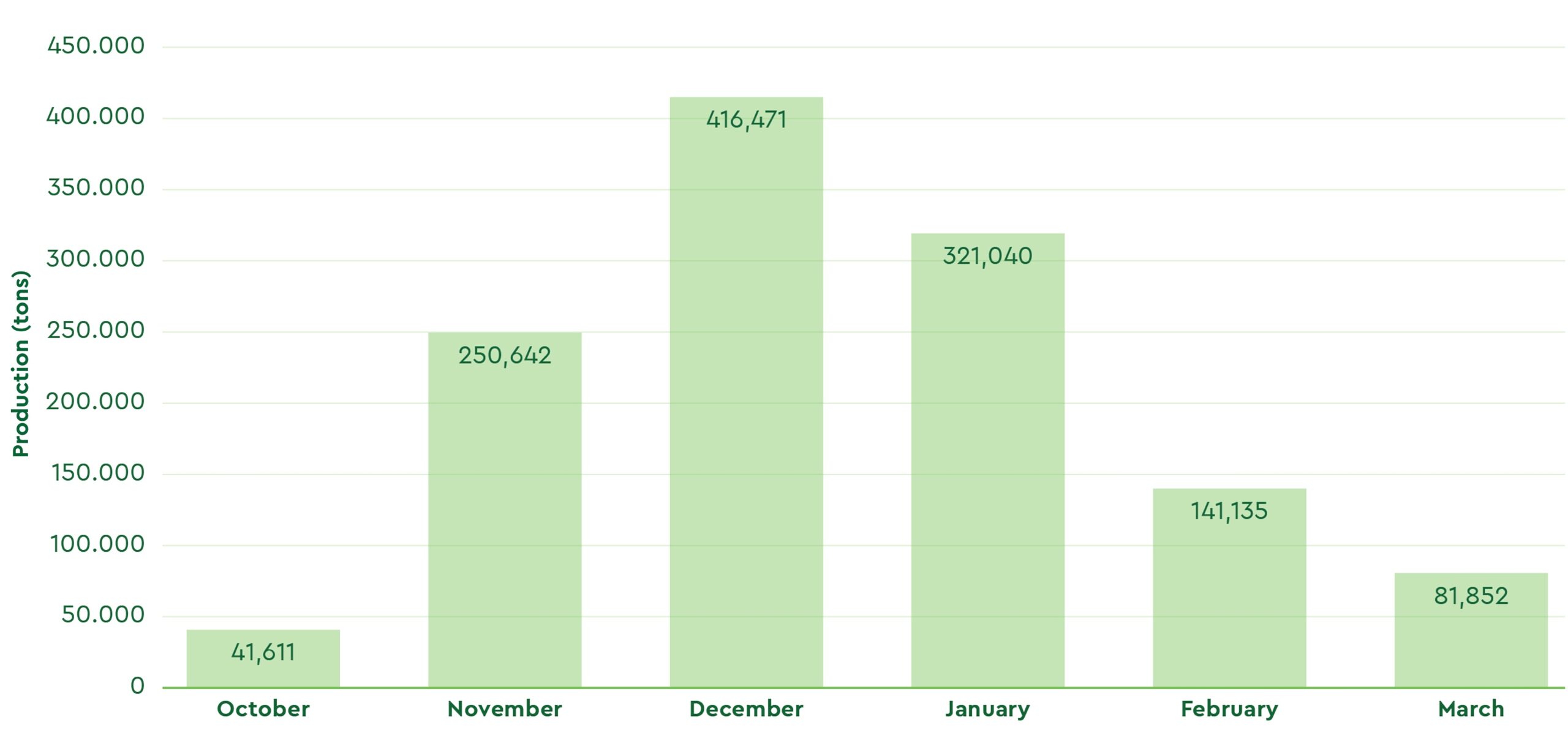

Cumulative Spanish production through March 2026 stands at 1.28 million tons, according to official Spanish Food Control and Information Agency (AICA) data. While this confirms a recovery from previous low-yield cycles, the total remains 7% below the initial forecast of 1.37 million tons. Milling activity in March yielded 81,852 tons, indicating the conclusion of the 2025/26 harvest.

Olive Oil Production in Spain 2025 – 2026 Season

Source: Wikifarmer

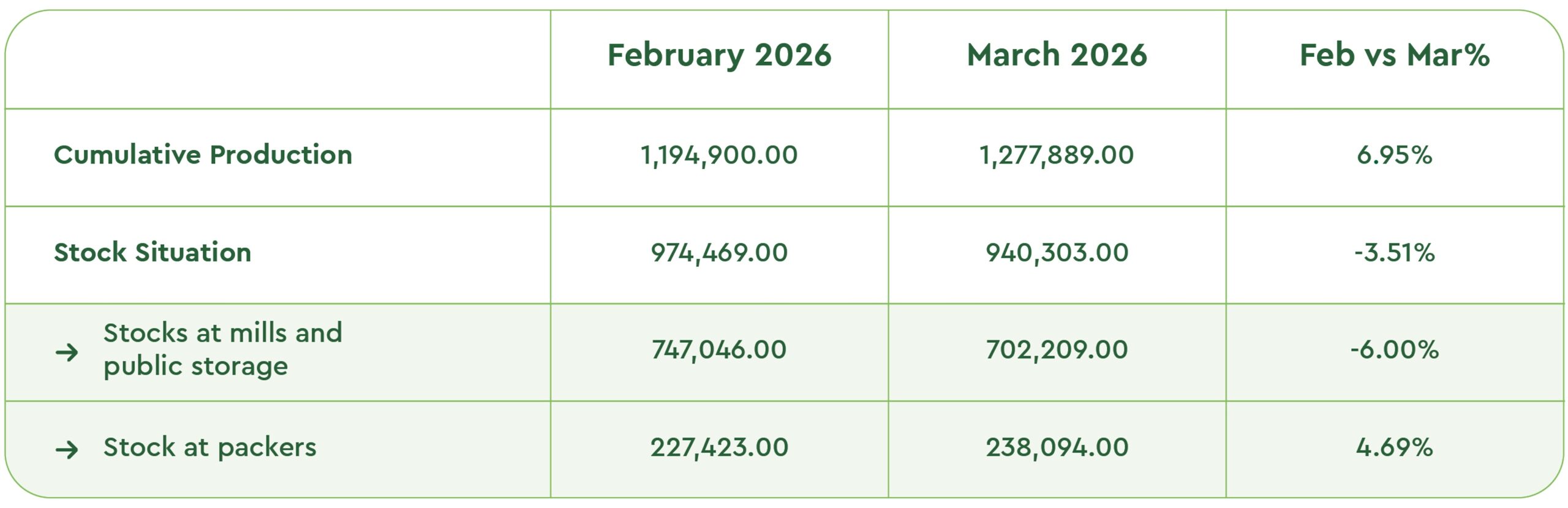

The market demand remains sustained, as evidenced by a total sale volume of 118,982 tons (domestic and export) recorded in March alone. This strong outflow is reflected in the shifting stock levels across the supply chain:

- Mill Stocks: Stocks held at the mills fell to 692,616 tons, representing a sharp decrease of 46,339 tons compared to February. This confirms a significant movement of bulk oil into the market.

- Bottler Stocks: In contrast, stocks at the packaging and bottling level increased to 238,094 tons (a rise of 10,671 tons), highlighting continuous packaging activity to meet steady consumer demand.

By the end of March, total industry stocks reached 940,303 tons.

Recent data released by the Italian Ministry of Agriculture (MASAF) and the ICQRF Frantoio Italia report indicate that olive oil stocks in Italy have risen significantly. Total inventories now stand at approximately 304,393 tons, representing a 42.9% increase year-on-year. This growth reflects a recovery in Mediterranean production volumes and shifting inventory management strategies.

The largest share of these holdings consists of Extra Virgin Olive Oil (EVOO), confirming its dominant role in the Italian origin market and the structural concentration on high-quality tier production. While this indicates a period of supply recovery following previous harvest variability, the balance sheet remains sensitive. Market analysis from Olive Oil Times and Assitol highlights that Italy is entering the 2026/27 cycle with thin margins and renewed volatility.

High production costs, especially labor and energy, along with structural supply imbalances continue to shape the sector. With its status as a leading producer and home of many global olive oil brands, Italy’s domestic output, averaging 250,000–300,000 tons, remains structurally insufficient to meet a national demand of 550,000 tons and export commitments of 400,000 tons.

This persistent production deficit necessitates a continued reliance on strategic import flows, primarily from Spain, Italy’s leading intra-EU trade partner, and Tunisia. As a primary re-export hub, Italy’s market equilibrium is fundamentally tied to the availability of Mediterranean bulk oils, making the upcoming 2026/27 harvest cycle critical for maintaining global supply chains.

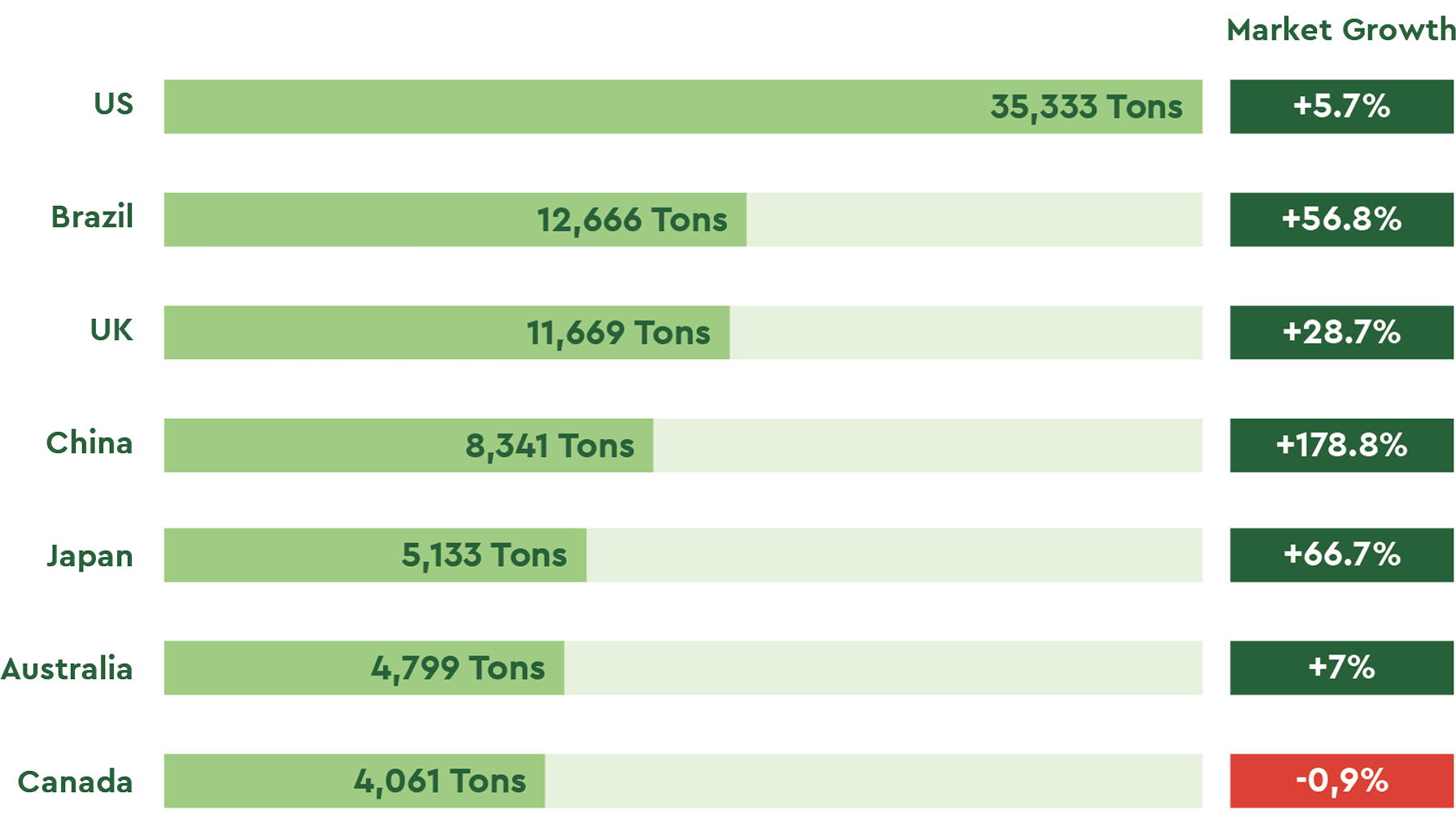

EU Trade: Olive Oil Exports up 11.6%, Driven by China and Brazil

An interesting article from Mercacei, a Spanish industry media outlet focused on the olive oil sector, reports that European olive oil exports increased by 11.6% during the first four months of the 2025/26 campaign. A total of 120,406 tons were exported to third countries, confirming strong and sustained international demand.

The United States remains the largest market with 35,333 tons (+5.7%), followed by Brazil with 12,666 tons (+56.8%) and the United Kingdom with 11,669 tons (+28.7%). Both Brazil and the UK show particularly strong growth.

Asian markets stand out for their rapid expansion. China imported 8,341 tons (+178.8%), while Japan reached 5,133 tons (+66.7%). Other markets remain relatively stable, with Australia at 4,799 tons (+7%) and Canada at 4,061 tons (-0.9%).

European olive oil exports are experiencing robust growth overall, with rising demand from China and Brazil acting as key drivers that are increasingly influencing global trade dynamics.

Italy: Northward Acreage Expansion and Risk Diversification

Recent reports from ISMEA and Olimerca confirm a structural expansion of olive cultivation in Northern Italy. Driven by climate shifts and farm diversification, olive acreage is increasingly replacing traditional vineyards and orchards in regions previously considered marginal for the sector.

Data indicates significant growth between 2020 and 2023, led by Piedmont (+40%) and Friuli-Venezia Giulia (+16%). In Trentino-Alto Adige, cultivation has surpassed 400 hectares, primarily concentrated around the Lake Garda microclimate. Growers are prioritizing cold-hardy, high-quality cultivars including Casaliva, Frantoio, and Leccino. While current climate conditions facilitate this northward shift, historical records indicate this trend represents a return to ancestral cultivation patterns in the Alpine foothills.

This expansion offers significant strategic benefits for the Italian olive sector. By establishing production hubs in more temperate northern microclimates with superior water availability, the industry can mitigate the systemic climate risks affecting Southern Italy, where drought and extreme heat increasingly impact annual yields.

This geographic diversification acts as a stabilizer for national production cycles, spreading risk across a broader climatic range.

Final Thoughts for 2026 Strategic Procurement: The Value Discovery Phase

The 2026 market landscape is defined by a significant shift in the global production hierarchy.

According to the International Olive Council (IOC), Tunisia has officially overtaken Italy and Greece to become the world’s second-largest producer, with a 2025/26 harvest estimated at 450,000 tonnes (+32% YoY).

This surge provides a volume cushion for global buyers, as Tunisian bulk oils continue to offer a competitive alternative to European origins. For global retail buyers, the strategy for 2026 will prioritize diversification, particularly as the trade regulatory environment in North America and the EU evolves.

The 2026 expiration of the current temporary 10% U.S. tariffs coincides with new Department of Commerce investigations that are likely to yield new, permanent duties. This shift, alongside potential tax refunds from the U.S. government, creates a complex fiscal environment that might favor players with flexible, multi-origin supply chains and diversified market strategies.

Simultaneously, the EU is expanding global access through landmark trade deals. The EU-Mercosur agreement, opened in 2026, protects 350+ Geographical Indications across a market of 800 million, while new agreements with Australia and Chile eliminate nearly all agri-food tariffs. These pacts go beyond reducing trade costs, legally entrenching European quality standards and GI protections across Oceania and Latin America.

The 11.6% rise in European exports, largely absorbed by China and Brazil, indicates that North American and Asian buyers are now competing more directly for the same Spanish pools.

Procurement teams should watch the ongoing harvests in Chile and Argentina (Q2 2026) as a secondary hedge to stabilize inventory before the European 2026/27 harvest enters the “Price Discovery Phase.”

Our team will be at the PLMA World of Private Label in Amsterdam on May 19–20, 2026 (Hall 7, N.39). We invite global buyers to schedule a meeting to discuss multi-origin sourcing strategies, tariff mitigation, and how to leverage these new trade opportunities for private label resilience in the 2026/27 cycle.

Share on